We have a major language problem in impact investing, one that speaks to how nascent we are in really understanding and segmenting our marketplace.

The two main classification systems we have adopted are:

- “Finance-first” and “impact first,” formally coined by the Monitor Institute in 2009

- “At market” and “below market” rates of return

Of course, in order to talk about “at market” or “below market” rates of return, one must have a reference point in mind. One can only be “at” or “below” a market if a market exists.

So what is that market? In the way we’re using language today, things feel quite loose, with the unstated assumption that the “market” of reference is developing world private equity investing. If that’s the implication, it feels equivalent to conceding that “impact investing” is nothing more than old wine in new bottles, which would vastly understate its potential. To put a more positive spin on things, we’ll know that impact investing is at a different place – and not simply looking outside the sector for its benchmarks – when the fact that a fund is “impact-” or “finance-first” doesn’t ipso facto tell you what targeted financial returns should be. To figure that out, you’d need to dig much deeper into investment strategy, including segmentation by sector or geography or customer base.

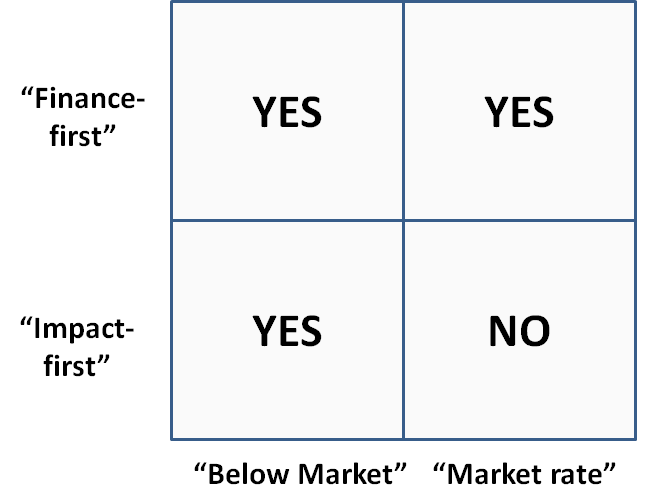

To clarify, let’s boil this down to a simple 2×2, with “impact” or “finance-first” on one axis and “at market” or “below” market on the other.

Which Markets Exist?

The way we are using language, I’d posit that we have an empty box (the “NO” below) in “market rate” “impact first” investing. We’re acting as if there is literally no such thing as “at market” with an impact-first orientation. This in turn implies that there is no market for impact-first investing. Troubling indeed.

I of all people am a huge fan of simple language, but I think we’ve settled on the wrong terms in pursuit of simplicity. What we’re really trying to say is that the level of financial return that would adequately compensate an investor for the risk she is taking in a pioneering impact-first investment would have to be astronomically high – 30%, 40%, even 50% IRRs – to compensate for the risk of investing in new, untested business models. In fact, if you think about it, since most impact-first investments are in areas that are unproven (and, therefore, much riskier), one would have to deliver even higher financial returns for “impact first” investments to adequately compensate investors for the risks they are taking.

Unless…

Unless social return has real value. Unless that value can be clearly quantified and communicated. Unless we can start segmenting the marketplace to say that “here and here and here and here we are building a market, and that takes time and money, so for now the expected financial returns are low.”

“Low,” but not “below market.”