[Note: this post originally appeared on the Acumen blog]

Today, the World Economic Forum (WEF) is releasing a new report titled, From the Margins to the Mainstream: Assessment of the Impact Investment Sector and Opportunities to Engage Mainstream Investors. The report aims, in the author’s words, to “provide an initial assessment of the sector and identify the factors constraining the acceleration of capital into the field of impact investing.”

The report serves as a field guide for anyone looking to allocate capital into impact investing, targeting in particular the mainstream providers of capital (e.g. pension funds) that are, by and large, sitting on the sidelines.

Unlike some of the previous comprehensive reports on impact investing, the WEF report avoids the temptation of contributing to the hype around impact investing. Rather, the authors, Michael Drexler and Abigail Noble, working in collaboration with Deloitte Touche Tohmatsu, provide a clear-eyed assessment of the state of the market today, collecting and clearly presenting much of the available aggregate data for the sector and also speaking directly to those who are managing mainstream institutional capital to understand how they view impact investing and what it would take for them to deploy capital into the space.

Clarifying Definitions

This report will serve as a powerful jumping-off point for the next stage of conversations within impact investing, and also, I hope, will accomplish the not-so-small goals of putting behind us the definitional questions of “what do we mean by impact investing” and “is impact investing an asset class?”

Let’s start with the definition of impact investing. The WEF working group on impact investing, of which I was a member, started by wrestling with this core definitional question, and, as usual, the group was split between debate on the substance of the definition and fatigue that we still, as a sector, are stuck returning to first principles. Indeed, between the GIIN, ANDE, leading practitioners like Pierre Omidyar and Matt Bannick, JP Morgan Social Finance, and the G8 Social Investing Forum we still don’t have an agreed-upon definition of impact investing. Hopefully, with this report, those days are behind us.

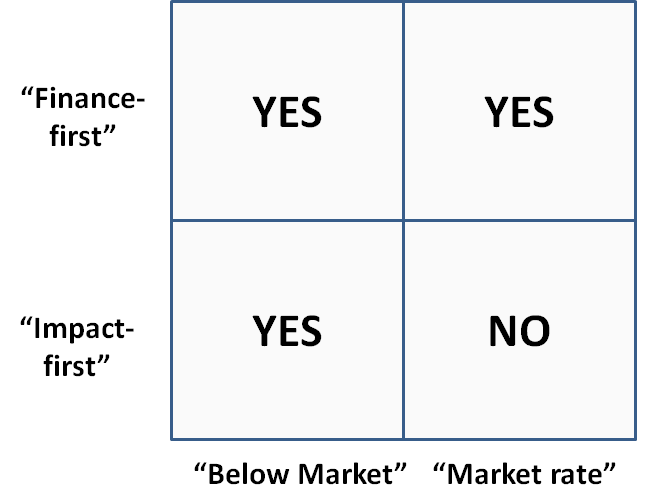

The report defines impact investing, simply, as “an investment approach that intentionally seeks to create both financial return and positive social or environmental impact that is actively measured.” The notable words in this definition are “intentionally” and “actively measured” – for how can we be impact investors if we do not intend to create impact, and how can we know if we have created impact if we do not actively measure what we have accomplished in both financial and social terms? What unites impact investors is a shared purpose (“intention”) in creating social impact, and all the diversity of investment theses, sector focus, and expected risk / return profile should not obscure this fact. And, as a sector we must set minimum standards around social impact measurement, and continue to drive the practice of assessing the social impact, in order to demonstrate to ourselves and to the world where and how we are making a difference.

The WEF report also quickly and elegantly dismisses the notion that impact investing is or should be an asset class, stating that impact investing “is a criterion by which investments are made across asset classes. An asset class is traditionally defined as securities or investments that behave similarly under varying market conditions and that are governed by a similar set of rules and regulations. Under this definition, it is clear that impact investing is an investment approach across asset classes, or a lens through which investment decisions are made, and not a stand-alone asset class.” Hopefully this succinct statement, and the supporting arguments in the report, will put this question to bed once and for all.

The Perspective of Mainstream Investors

To date, according to the WEF report (sourcing 2012 data from GIIN and JP Morgan), the largest providers of capital into impact investing to date are Family Offices/High Net Worth Individuals and Development Finance Institutions (DFIs) – which is surprising since together Family Offices and DFIs hold just 2.5% of all global assets. The goal of the WEF report is to demystify impact investing for the holders of the other 97.5% of global assets, and the authors started by talking to these holders of capital to see what they think of impact investing today. The results of these conversations are quite sobering. For example, in surveying representatives of US-based pension funds the authors discovered that:

[The WEF] survey results indicate that US-based pension funds are generally unfamiliar and confused by the term “impact investing.” Almost all (81%) of the respondents have heard of the term before, but most feel that it is another term for responsible or sustainable investing (36%) or that it is a noble way to lose money (32%). Only 9% felt that impact investing is a viable investment approach. As such, only 6% of respondents are currently making impact investments today.

The question, of course, is whether these U.S.-based pension fund managers are missing something or if, instead, we are in the early days of impact investing and it is appropriate for mainstream capital to, by and large, be sitting on the sidelines.

One telling piece of data from the report is that of the 242 impact investing funds assessed in April 2013, 62% of these funds had less than a three year track record, indicating that it is very early days in this market. Furthermore, much of the capital in the market today, especially capital outside of microfinance funds, is deployed in long-term, illiquid investments, so it should not be surprising that mainstream investors are taking a wait-and-see attitude since financial returns for most fund managers are largely unrealized. On the flip side, these data reinforce that, for those who are willing to take on risk and be first movers in this space, there are tremendous opportunities.

Recommendations

The WEF report ends with a series of recommendations around what it will take to accelerate the growth of the impact investing ecosystem and, in turn, bring more mainstream capital into the space. These recommendations – three each for impact investment funds, impact enterprises, philanthropists and foundations, governments, and intermediaries – are the most actionable part of the report for those of us in the sector, and they should be taken seriously. The recommendations that strike me as the most important are:

- For impact investing funds: be clear and transparent about financial returns and standardize impact reporting. In this next phase of development of our sector, we have an urgent need for segmentation, and this will not be possible without real data. It is up to all impact investors to build the systems to collect data on financial and social performance, and take the steps to share it, so that the world can develop a much better understanding of actual rather than targeted performance.

- For impact enterprises: proactively measure and report on social and environmental impact. It is up to the sector as a whole to standardize measurement practices and to bring the costs of measurement down, and up to leading impact enterprises – especially those first movers who have reached scale – to show what is possible in terms of measuring and sharing social and environmental impact data. We need these success stories to show us the way.

- For philanthropists and foundations: Help lower risk by providing grants to early-stage enterprises and anchor investments to impact investment products and funds. Given how much capital is still sitting on the sidelines, as well as the fact that philanthropists and foundations have been the first movers in this space, we need continued deployment of risk capital (grants and subordinated capital) – to companies and to funds – from those who understand the space best.

- For governments: Help de-risk the ecosystem through innovative financing mechanisms. Whether through guarantees (like the New York Acquisition Fund), subordinated positions in funds, or other mechanisms (e.g. Social Impact Bonds or Development Impact Bonds), governments can use their capital to accelerate the growth of the sector and attract mainstream capital. Impact investing is creating public goods and governments should be comfortable using public monies to accelerate the growth of this ecosystem – including by luring in mainstream financial players.

- For intermediaries: aggregate data on impact investing and publish the findings. This is the clear corollary to the first recommendation. Our sector urgently needs real, available, public data on financial and social performance across different investment strategies, sectors, stage of investment and geography, in order to better discern the realities on the ground.

This WEF report is comprehensive, clear, and actionable, providing a tremendous opportunity for all actors in the space to accelerate the development of the impact investing ecosystem. It is exciting to see how far we have come, as well as to have a better sense of the next building blocks we will need to put in place to continue to grow and deepen the impact of our sector.